Biotech financing: darkest before the dawn

Technology tamfitronics After a difficult three years, biotech financing may slowly be returning to health.

Credit: Norman Price / Alamy Stock Photo

“It was the best of times, it was the worst of times,” wrote Charles Dickens in A Tale of Two Cities. The same might be said for biotech financing today.

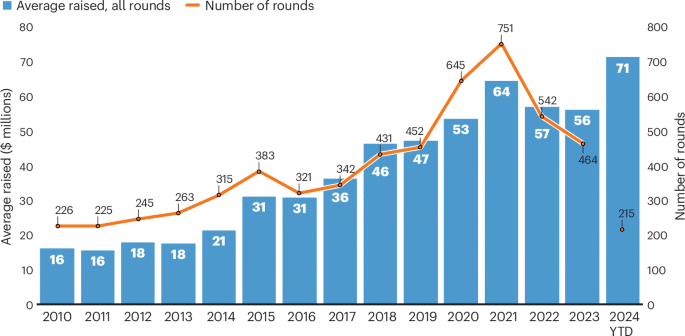

On the plus side: flourishing innovation, robust mergers and acquisitions (M&A) activity, and average private biotech funding round sizes at a 15-year high (Fig. 1) On the downside: stubbornly muted public markets and cautious, choosy venture capitalists (VCs) struggling to raise their own new funds in “the worst [environment] I have ever seen” for VC fundraising, according to Antoine Papiernik, chairman and managing partner at Sofinnova. Most biotechs are stuck in a deep, long-lasting downcycle.

Average venture funding round size reaches an all-time-high in the first half of 2024. YTD, year to date. Source: DealForma Database.

Most — but not all. Three years since the start of its fall from record-breaking pandemic peaks, biotech remains a sector of wildly divergent fortunes (see Nat. Biotechnol. 41597–603, 2023; Nat. Biotechnol. 40450–457, 2022; Nat. Biotechnol. 39408–413, 2021). The fat cats: companies with — and investors in — clinical-stage assets on big pharma’s acquisition radars, or management teams with a strong track record. The paupers: earlier-stage groups for whom the music stopped before proof of concept.

Capitalism drives a widening wedge between haves and have-nots. Investors and companies on the right side of the line “can attract funds, talent and entrepreneurs,” says Sander Slootweg, managing partner at Naarden, Netherlands-based VC firm Forbion, itself flush with proceeds from six-billion-dollar-plus portfolio company acquisitions by big pharma within the last 14 months. Experienced teams working in hot therapy areas are raising outsized rounds — like the $400 million in March 2024 for immuno-inflammation startup Mirador Therapeutics, founded by Mark McKenna, former CEO at Prometheus Biosciences (the latter of which was acquired by Merck & Co. for $10.8 billion in 2023). Neuropsychiatry-focused Seaport Therapeutics launched the following month with $100 million. It is founded and run by Daphne Zohar, co-founder of Karuna (acquired by Bristol Myers Squibb for $14 billion in late 2023). Cancer-focused Synnovation Therapeutics, which raised a $102 million series A in January, is run by a team with experience developing kinase inhibitors at Incyte.

Those biotechs and investors left behind — including the early-stage, the new and the unlucky — must streamline, refinance on less favorable terms, merge or shut down. “Financing early-stage innovation has been very challenging,” says David Schilansky, co-founder and CEO of European seed financier and biotech builder Home Biosciences.

Signs of a new dawn may be emerging. Central nervous system (CNS)-focused Rapport Therapeutics’ $174-million June initial public offering (IPO) was one of few to trade upwards, and the queue to list is lengthening. Biotech IPOs in 2024 remain rare, but sums raised in the first half of the year already surpass 2022 and 2023 (Fig. 2a). Corporate VC is stepping up to support early-stage innovation, pushing overall biopharma VC financing to a projected $28 billion for the full year (Fig. 2b). That total won’t beat frothy 2020 or 2021, but still represents healthy growth from pre-pandemic 2019.

aBiotech IPOs remain scarce so far in 2024, but sums raised beat the dismal totals for 2022 and 2023. bTotal biopharma venture funding in 2024 is on track to surpass pre-pandemic (2019) levels. YTD, year to date. Source: DealForma Database.

Selected VCs are in fact raising new funds: Flagship Pioneering raised one worth $3.6 billion in July, following Foresite Capital’s $900-million biotech-focused fund that closed in June 2024. SEC filings suggest a multi-billion-dollar raise is also underway at Arch Venture Partners. Assuming VC fundraising continues at this rate for the rest of the year, 2024 would see $20 billion in new biotech-focused funds, according to investment bank Stifel. That’s below 2021’s peaky $31 billion, but still a substantial step up from the previous decade.

Big pharma companies, meanwhile, still have about $1 trillion to spend, according to a recent Ernst & Young reportmaking them biotech’s best friend as public markets remain tight. Some drugs giants urgently need to fill large sales gaps as best-selling drugs including Merck’s Keytruda lose patent protection this decade. Others, like Novo Nordisk and Eli Lilly, are being showered with cash from their respective obesity/diabetes franchises, Wegovy/Ozempic (semaglutide) and Zepbound/Mounjaro (tirzepatide). Biotechs that “align themselves with what [big pharmas] need have a good chance” of success, says Papiernik.

Finally, interest rates — whose rise since the end of 2021 has lured investors away from risky assets like biotech — now appear flat or downward-trending. “It doesn’t feel good if you’re a small biotech trying to raise money, but things are going in the right direction,” says Allan Marchington, head of life sciences at investment company ICG in London. “We’re climbing out of it.”

Bigger winners, faster

Biotech financing rounds are fewer, but larger: the average private financing round so far in 2024 (excluding seed rounds) is almost $90 million (Fig. 3a), and at least 50 companies have raised rounds worth $100 million so far this year, according to Endpoints.

aSo far 2024 has seen fewer, larger biotech financing rounds. bIn 2024 so far, the average A round is worth $80 million — more than double the average in 2019. YTD, year to date. Source: DealForma Database.

One reason for this winner-takes-all landscape is investors’ preference for later-stage programs. This mirrors big pharma’s chase for assets in large, competitive markets like obesity, autoimmune diseases and neurology, big enough to fill revenue holes left by older drugs. Pharma buyers want clear evidence of clinical differentiation, forcing VCs to fund companies for longer, and more generously. “We are now in a world where more VC is going into clinical than preclinical assets,” says Tim Haines, executive partner at VC firm Abingworth — a trend likely to continue if public markets remain fragile. (In 2019, it was the reverse: more VC went to preclinical and platforms than clinical-stage companies.) Growing VC fund sizes also encourage bigger rounds: managing dozens of smaller deals is too resource intensive.

So far in 2024, a quarter of all series A rounds are worth over $100 million, and the average A round is $80 million — more than double the average five years ago (Fig. 3b). This takes pressure off raising additional money in a series B or C, says Haines.

Many of these series A rounds support companies that have in-licensed clinical assets in attractive therapy areas and are helmed by experienced management teams. Cancer still dominates the VC totals, but “those in areas like obesity, neurology, immunology or AI can get oversubscribed rounds” says Naveed Siddiqi, senior partner of venture investments at Novo Holdings (Fig. 4).

Cancer still draws the lion’s share of VC funding, but neurology, endocrinology and autoimmune diseases are increasingly popular. YTD, year to date. Source: DealForma Database.

The obesity gold rush spearheaded by Novo and Lilly’s GLP-1 agonist-based therapies semaglutide and tirzepatide is luring investors: Metsera emerged in April 2024 with a pipeline of in-licensed obesity assets and $290 million seed and series A funding led by Arch Venture Partners and Population Health Partners. Hercules CM NewCo attracted $400 million from Bain, RTW and Atlas Venture for a pipeline of GLP-1-based assets in-licensed from China. Third Rock Ventures-incubated Marea Therapeutics launched in mid-June, attracting $190 million (series A and B) to progress a ANGPTL4-targeting antibody licensed from Novartis that is already in phase 2 for metabolic dysfunction.

Newly listed Rapport emerged in 2023 with a clinical asset from Johnson & Johnson for seizure disorders; it raised a $100 million series A and a further $150 million series B within weeks, capitalizing on resurgent interest in CNS drugs. The founding team came from Cerevel Therapeutics, now part of AbbVie. Amsterdam-based VectorY Therapeutics raised a $138 million series A to progress its adeno-associated virus (AAV)-delivered antibody into the clinic for the rare neurodegenerative condition amyotrophic lateral sclerosis. VectorY is run by co-founder Sander van Deventer, who also co-founded gene therapy company uniQure and VC firm Forbion, which built VectorY and co-led the financing.

Immunology is another jackpot area for potential buyers. London-based VC firm Medicxi assembled six immunodermatology-focused portfolio companies plus $100 million to create Alys Pharmaceuticals in February 2024. Inflammation and immunology are “attracting huge interest from pharma,” says partner Francesco de Rubertis, given the multiple indications and pathways in the space. “Obesity is hot, but much harder to break into” if you’re not already a player, he says.

Seed rounds inflate

Fewer, bigger A rounds mean fewer, bigger seed rounds. “We need to put more time, effort and money into seed projects, to ensure our companies are among the ‘haves’” in attracting follow-on funding, explains Søren Møller, managing partner at Novo Seeds in Copenhagen. It’s a similar story at company builder Third Rock: “We’re keeping companies inside for longer, so that when they do emerge, they’re closer to the line,” says Third Rock partner Jeff Tong. (Third Rock company Marea was founded in 2020, four years before launch, to explore new categories of cardiometabolic drugs.)

Bigger seed rounds aren’t all for asset-focused groups. The right platforms — combined with the right teams — can also win. Orbis Medicines’ macrocycle-based technology attracted a $28 million seed investment from Novo and Forbion in February, surpassing the more typical E8-12 million round size. Orbis’s oral macrocycle drugs, based on cyclic scaffolds composed of 4 or 5 amino acids, have wide application across disease areas. Their flexibility and targeting precision also appeal to those developing multicomponent modalities such as antibody–drug conjugates (ADCs) and radioligand therapies (RLTs).

Management track record is a prominent feature of today’s bifurcated landscape: investors putting larger sums of money to work want to back tried-and-tested teams. Orbis co-founder and board member Christian Heinis, associate professor at Ecole Polytechnique fédérale de Lausanne, is also behind Nasdaq-listed Bicycle Therapeutics, whose looped peptides, designed to combine the best attributes of biologics and small molecules, helped Bicycle raise one of the year’s biggest private investments in public equity (PIPEs), worth over half a billion dollars.

Modality matters: ADC, not CGT

Those working in hot spots like ADCs can buck investors’ ‘clinical assets only’ rule. Munich, Germany-based Tubulis raised $139 million in March to advance its cancer-focused ADCs toward proof of concept. (The first patient in a phase 1/2a ovarian cancer trial was dosed in June.) Preclinical Pheon Therapeutics raised $120 million in May 2024. Investors see big pharma’s appetite for ADCs: there was several tens of billions worth of ADC-focused M&A and partnership activity in 2023, including Pfizer’s $43-billion acquisition of Seagen and AbbVie’s $10-billion deal for ImmunoGen. The action continues this year, with Johnson & Johnson’s $2-billion Ambrx purchase and Genmab’s $1.8-billion deal for ProfoundBio.

Companies working on RLTs — radioactive isotopes attached to cancer-targeting ligands — are also in the winners’ camp. Positive data from Novartis’s marketed Lutathera (lutetium-177 dotatate) for gastroenteropancreatic neuroendocrine tumors and Pluvicto (lutetium-177 vipivotide tetraxetan) in metastatic prostate cancer have drawn attention to RLT’s attributes. They are less prone to typical drug resistance mechanisms, as some radiation shreds both DNA strands, leaving little room for genomic alterations that can allow cancer cells to outmaneuver toxic rays. RLTs can also offer a unique ‘see what you treat’ quality, since isotopes can be tracked using nuclear imaging tools.

New isotopes and conjugation chemistries are driving an expanding RLT pipeline and financings to match (Table 1 and Nat. Biotechnol. 421003–1008, 2024).

Cell and gene therapy (CGT) companies are faring less well. Venture totals, number of financings and average round size are all down steeply, reflecting clinical, manufacturing and commercial hurdles (Fig. 5a) “We expected to have figured out manufacturing and scalability by now, but we’re not there yet,” said Miquel Vila-Perelló, co-founder and CEO of gene therapy player SpliceBio at a conference in April. “It has been more complex than we could have imagined,” added Arnaud Autret, principal and head of European operations at Illumina Ventures.

aVenture funding for cell and gene therapy has plummeted in 2024, reflecting clinical, manufacturing and commercial hurdles. bCompanies using AI or machine learning for healthcare research and drug discovery are on track to raise more venture money in 2024 than in any previous year apart from 2021. YTD, year to date. Source: DealForma Database.

To win funding in this space requires clinical data. London-based Beacon Therapeutics raised a $170 million B round in July 2024 to progress its lead phase 2/3 gene therapy for X-linked retinitis pigmentosa. Forbion led the round, supported by existing investors including London-based Syncona, which was previously heavily focused on CGT but has since broadened its scope.

Artificial intelligence (AI) continues to sweep across biopharma — not as a new modality per se, but promising to transform everything from drug design to patient selection and care delivery and driving a broader investment frenzy. Xaira Therapeutics, whose ambition is to upend R&D with AI, drew in a chart-topping $1 billion A round in April 2024 from co-incubators Arch Venture Partners and Foresite Labs plus a dozen more investors. This was the largest initial funding commitment in Arch’s history, according to Xaira managing director and co-founder Robert Nelsen. Xaira is less biotech startup than coalition of top scientists, drug developers and disruptive platforms.

AI is also drawing tech investors to biotech. AI-powered protein design company EvolutionaryScale, founded in June 2024 by former Meta scientists, raised a $142-million seed round from tech investors including Amazon Web Services and the venture arm of chip-maker Nvidia. Companies using AI and machine learning for healthcare research and drug discovery are on track to raise more venture money in 2024 than in any previous year apart from 2021 (Fig. 5b).

Tough choices for those in the middle

For most biotechs — that is, those not raising larger-than-average seed or A rounds — it’s a difficult time. Many seeking series B or C funding are forced to accept lower valuations than in their earlier, pandemic-inflated rounds, particularly if they lack proof-of-concept data. This explains why existing VCs have lost money and why those VCs’ backers — limited partners — are reluctant to contribute to new funds (Box 1). “Investors in preclinical or early-clinical-stage deals are still very selective,” says Roel Bulthuis, managing partner at Syncona.

This middle ground between startup and clinical validation is where the legacy of pandemic exuberance has hit hardest. And it hasn’t yet fully played out. Until the start of 2024, some investors had sufficient reserve funds to protect their private holdings with bridge rounds. “Nowadays, reserves are smaller,” says Sofinnova’s Papiernik. Valuation corrections — which were, in the immediate aftermath of the pandemic, visible only in the share prices of public biotechs — have now trickled down to private biotechs, as empty coffers force the reckoning that comes with a follow-on private round. In some cases, existing backers will swallow a lower valuation to keep the company going. Others may merge portfolio companies. Not all will make it.

“It’s time to choose. The cleanup is not done,” says Papiernik.

Despite the pain, veteran specialist investors mostly agree that a cull is welcome. Atlas Venture’s Bruce Booth in April 2024 welcomed the drop-off in startup creation during the first quarter of this year, citing the damage incurred when constrained talent is spread across too many companies. “Concentrating the scarce high-quality talent in fewer companies will collectively be a good thing for the sector,” he wrote on his Life Sci VC blog.

Corporate VC to the rescue in Europe

Some worry that the changing shape of VC, toward bigger funds and shorter investment cycles, may prove damaging in the long term. “Investors have alternatives — more advanced companies, with lower valuations — which is sucking money and attention away from early-stage companies that need money now,” says Syncona’s Bulthuis. The problem is particularly acute in Europe, which lacks the range of deep-pocketed company builders present in the United States (notwithstanding exceptions like Forbion-partnered BioGeneration Ventures, Novo Holdings’ Novo Seeds or Syncona).

Corporate VC is stepping up, though. When there’s less money around, “our phones start ringing,” says Hakan Goker, managing director of M Ventures, the venture arm of Darmstadt, Germany’s Merck KGaA. “It’s a cyclical love affair” between corporate and institutional investors, says Goker, but as the latter shift downstream, pharma firms’ investment arms have become particularly important for company creation and earlier-stage support. “They’re one of the few stable market participants,” says Bulthuis, who previously worked in corporate VC.

M Ventures and AbbVie Ventures both participated, alongside Sofinnova, in a $21.5 million seed round for Cologne, Germany-based Disco Pharmaceuticals in January 2024. Disco’s technology identifies cancer cell surface proteins at scale, unlocking new targets for the burgeoning ADC and bispecific antibody fields. The $37.8 million raised by Lund, Sweden-based preclinical immunotherapy company Asgard Therapeutics in March 2024 came almost exclusively from corporate VC and government funds, another stalwart of early-stage European investment. BMS Ventures in May became the latest participant in an extended financing round for preclinical Altrincham, UK-based NeoPhore, whose small molecule neoantigen-generating drugs are being positioned as next-generation cancer immunotherapies. BMS Ventures joined Astellas Venture Management and other non-pharma corporate VCs.

Lilly Ventures and Novo Ventures are particularly well placed to support the earlier-stage ecosystem, thanks to their parent companies’ obesity therapy windfalls. Novo Ventures has access to evergreen capital from parent Novo Holdings, which also owns Novo Nordisk, and has put over $300 million into biotech since January 2024. (Novo Holdings is part of the Novo Nordisk Foundation, one of biggest healthcare investors globally.)

The $2.2 billion raised by European biopharma and platform firms in the first half of 2024 puts the region on track to surpass all years except 2021 (Fig. 6a) But Europe still lacks later-stage funding. That’s where the gap with the United States is largest, according to Vanessa Carle, senior associate at Forbion, one of few European investors with a dedicated growth fund. Europe needs more growth funds because “when US investors come [to Europe]they often require a European lead” investor to help navigate the local funding and R&D environment.

aEuropean biopharma firms are on track to raise more venture funding in 2024 than in any previous year in the last decade and a half except 2021. bChinese biotech venture funding remains muted so far in 2024. YTD, year to date. Source: DealForma Database.

Tech-bio draws US investors to Europe

US investors are coming to Europe. Many are drawn by the tech-bio revolution to emerging hubs such as London, where Flagship Pioneering and OrbiMed both opened hubs in 2023. “London is becoming a real hub for ML/AI-enabled drug R&D companies,” says James Field, CEO and founder of London-based LabGenius, which is using machine learning to design and generate novel antibodies. M Ventures led a $44.6 million series B in May 2024.

US-based AI-powered drug hunter Recursion, whose $500 million IPO was 2021’s second-largest, recently announced plans to open offices in London’s King’s Cross, drawn to the area’s concentrated interdisciplinary talent across technology, biology and chemistry. The likes of Alphabet’s Google and DeepMind, Merck & Co., AstraZeneca and the Francis Crick Institute are all within walking distance; European blue-chip investors like Sofinnova, which launched a $200 million Digital Medicines fund in late 2023, also have a footprint here.

The UK government is actively promoting London’s rise as a biotech and AI hub, offering financial and policy support. In late 2023, it signed a memorandum of understanding to work with Flagship Pioneering to identify innovation opportunities, engage with national data repositories like UK Biobank, and find manufacturing sites for Flagship companies. Governments across Europe are stepping up efforts to boost local biotech (Box 2).

China: a “reservoir of opportunity”

China’s biotech sector has not escaped the woes facing its Western counterparts. IPOs are muted and an economic crisis has damaged VC investment (Fig. 6b). But as Chinese biopharmas shift from fast followers to innovators, there is “a reservoir of opportunity” for Western investors willing to navigate the geopolitical storm, says Medicxi’s de Rubertis.

The quality of Chinese assets is growing, yet they remain undervalued relative to their US counterparts, in part due to a lack of local capital. That’s attractive to Western investors seeking assets in crowded spaces. Lianyungang, China’s Jiangsu Hengrui Pharmaceuticals provided newly created Hercules CM NewCo’s clinical-stage GLP-1 based incretin assets, and also provided Aiolos Bio — acquired by GlaxoSmithKline in January for $1 billion — with a long-acting antibody to thymic stromal lymphopoietin in phase 2 for asthma. Genmab’s new ADC unit ProfoundBio, though headquartered in Seattle, was co-founded by a Chinese scientist and has R&D activities in China.

Medicxi in April 2024 led a $62 million series A+ round in Shanghai-based D3 Bio, whose phase 2 next-generation KRAS-G12C inhibitor could outshine Mirati Therapeutics’ (now Bristol Myers Squibbs’) Krazati (adagrasib). “We were so excited about the molecule that we wanted to invest” despite the political risk, says de Rubertis.

That risk is significant. Its most prominent manifestation is the US BIOSECURE Act, which seeks to curb or cut ties with Chinese companies in defense-sensitive sectors like biotech. The bill has not passed Congress yet, but experts expect it will. Western companies are already working out how to disentangle t hemselves from large contract development and manufacturing organizations like WuXi AppTec (also a shareholder in D3 Bio).

Still, Western investors find it hard to ignore what Genmab CEO Jan van de Winkel called, in a recent Financial Times article, China’s “mindbogglingly impressive innovation.” RTW in 2020 founded Shanghai-based Jixing Pharmaceuticals, which in-licenses Western assets to develop for the Chinese market. “Chinese innovation is catching up with that in the West,” said RTW partner Peter Fong at an event in December 2023. In the meantime, “we see an opportunity to bring technology to China and to build a global R&D center so that we are there when Chinese innovation does match” its Western counterpart.

Others are watching closely. “We actively scan for Chinese assets” that might improve existing mechanisms of action in fields of interest, including metabolic diseases, inflammation and immunology, and CNS, says Forbion’s Slootweg.

The new dawn

Given a dismal 2023, most agree with Novo Ventures’ Naveed Siddiqi that “things feel better now than this time last year.” How much better depends on where you’re sitting. The chosen few — biotechs and investors working in the right spaces, with the right experience — have more cash than ever and rich opportunities across the globe. The rest still face difficult times, as macroeconomic and geopolitical uncertainties continue to test investor confidence.

As biotech transitions from dark into dawn, Europe’s companies may prove more resilient than some of their US counterparts. “We’re better at getting along on less,” says Forbion’s Slootweg. European firms are accustomed to having little or no access to local public markets and to relying more heavily on M&A.

They may have to continue to work even harder to attract funding. The trend toward ever-larger — and thus more selective — financing rounds marks a “fundamental shift,” according to Rob Woodman, partner at Italian VC firm Panakès. “An $80 million financing round in Europe doesn’t stand out as much anymore.”

That is good news for the select European firms able to generate something sufficiently compelling to lure investors — especially US investors — from attractively priced US public companies. It’s less good news for the others.

Still, with recovery momentum building and as science surges forward, investors’ funding taps may start to open further. When they do, Siddiqi predicts, “it won’t take much for money to rush back in [to the sector]. We should not get stuck looking in the rearview mirror.”